Searching for professional accounting services that don’t leave you hanging?

ZERO Hidden Fees

Hundreds Of Happy Customers

Chartered & Certified Accountants

Strategic Management & Advice

And much more…

You Need An Accountancy Firm Who ACTUALLY Gets it!

When it comes to running your business, you put your all into it…

Whether it’s a side project or your livelihood, you want to make sure it succeeds. From your logo to your employees and from your finances to your building’s maintenance, no issue is a small issue and you take every bit of it seriously.

So when you realised that you needed to hire an accountant, you probably hoped to find a firm that felt the same way about your businesses as you do.

Unfortunately, you may have realised that’s more difficult than you originally thought…

We’re Not Your Typical Accountants…

We’ve heard so many horror stories of people signing on with a new accounting firm, only to find out that they’re not considered a priority, the pricing isn’t as transparent as they thought it was and their accounting is more reactive than proactive.

The most common complaints we hear are:

❌ They never answer their phone or emails.

❌ I’m not even really sure what they do for me.

❌ There are TOO many hidden fees

❌ They’re always busy with someone else’s work.

❌ Their other clients take priority because they’re larger businesses.

All Of Our Services Include

We’re committed to your success. Which is why all of our services cover the essentials you need to make your finances as easy and effortless as possible.

We can also create bespoke packages depending on your needs!

Fully Qualified Accountants

Our accountants are chartered and certified so you know your business is in safe hands.

Always 100% Transparency

We believe in 100% transparency which is why we have ZERO hidden fees or nasty surprises!

Expert Strategy & Planning

We don’t just stop at doing your accounts. We aim to help our clients become more profitable.

Jargon-free communications

We break everything down and explain things in a way that is easy and simple to follow.

Accountants Who Care

Forget what you think you know about accountants! We’re different!

Regardless of your terms of service, the package level that you’ve purchased, or the size of your company, customer service should be the top priority of any company that you partner with, especially when the finances of your company are at stake.

At Rodliffe, we took all of this in mind when founding our own Accounting Firm. We’ve set out to ensure that you’re able to find an accounting service that not only matches your needs but is also willing to treat your company as if it was their own.

Individuals

Limited Companies

“Well worth the fees, from when I arrived over 12 years ago, to now. I highly recommend David, Syed, and the Rodliffe team.”

“Fantastic. Efficient, knowledgeable, and supportive. Ensured our account transfer was seamless and delivered on every deadline without fuss. Exactly what every small business needs.”

“The team at Rodliffe Accounting has provided excellent financial planning advice to me and my business for the past 12 years.”

We Believe In 100% Transparency

Hidden costs, additional fees, excess charges…no thanks!

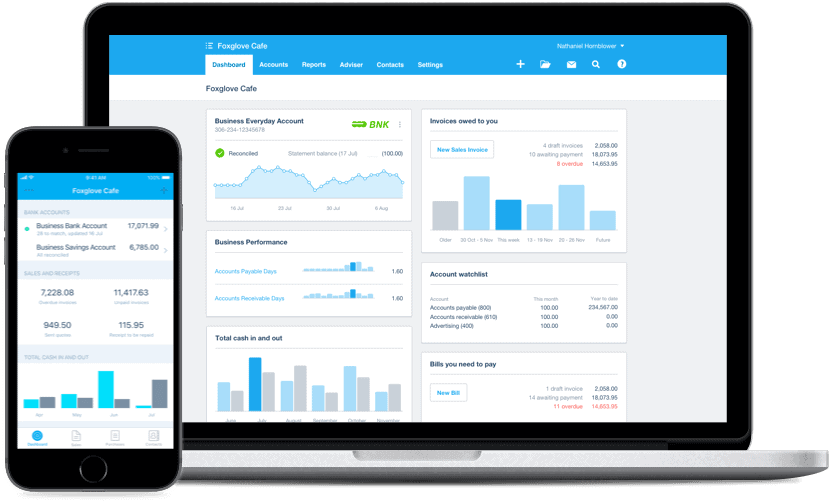

We do things differently! Pretty much all of the work we do is done via cloud accounting software, meaning you always have full visibility over what’s being done on your account.

We also offer simple fixed monthly pricing dependent on your needs, so you never have to worry about hidden fees or charges.

Ease The Pressure With

Cloud Accounting

Luckily for you, we’re different from a lot of accounting firms out there.

We believe in always looking forward; as such, we use cloud-based accounting software to save you both time AND money.

We’re also FreeAgent Platinum Partners and Xero Gold Partners, so we’re fully certified to set up and advise on these platforms.

We’ll also help you find the right software that plugs directly into your current operation with minimal friction.

Save Tax, Increase Profits

We offer a wide range of services that can be customized to fit your specific business needs. In addition, because we’ve worked with a variety of industries and business sizes, we’re able to grow right alongside you, ensuring that you’ve always got the resources you need to continue to thrive in your industry, regardless of how quickly you grow.

Ready To Get Your Time Back So You Can Focus On Growing Your Business?

You’re In Safe Hands With Us

Years Of Experience

Clients Served

Companies Formed

In Turnover Managed

Our Partners

What Our Customers Say…

“Rodliffe Accounting is an excellent accounting firm going above and beyond for their customers from day one! The team is always professional, knowledgeable and extremely helpful.”

Why Choose Rodliffe?

We Save You Money

Are you leaving money on the table? We work with our clients to ensure they’re not spending more than they need to on tax. We’ll also help you to identify other areas of the business that could potentially save you thousands each year.

Here When You Need Us

When we say we’re here for you; we mean it! We pride ourselves on being responsive and attentive to our customers. We’re only ever a phone call or email away. Better still, we’re always around for a coffee! ☕

Cloud Accounting

Say goodbye to hours of manual paperwork and painful reconciliation. We’ll work with you to find the right software solutions that effortlessly plug into your business, so you can get back to doing what you love!

The COVID-19 Financial Support Guide

The COVID-19 lockdown hit a lot of businesses hard.

As such, we’ve prepared a series of tips to ensure your business and team get all the support you need during these challenging times.

Vat Guidance

Job Retention & Furlough

Government Grants & Support

Challenge Us To Find The Hidden Profits In Your Business!

We get it, you’re not exactly short on choice these days…

That’s why we aim to blow you away with the amount of value we deliver upfront before we’d even consider asking you to become a customer!

It doesn’t matter if you’re just getting started, are a small or medium-sized business, or are already well on your way to success; we’ll dive right in and find those hidden profits and ensure that you never run into late fees or compliance issues.

But we can’t do any of that unless you make the first move and reach out.

All you’ve got to do is click that button below to get started.

© Rodliffe Accounting Limited 2020

Registered in England and Wales No. Company number 05673296